What You’ll Learn

What qualifies as an investment property from a lender’s perspective

Why loans for investment properties have higher interest rates

Minimum qualification requirements for investment property mortgage

Every big fish in real estate started off with just one investment property. If you’re thinking of dipping your toe in the water, it’s helpful to know exactly what qualifies as an investment property. You see, second homes can sometimes be classified as investment properties if they’re within 50 miles of your primary residence. This article isn't about property to relax in, it’s about property that works to make money.

From a lender’s point of view, there are 2 ways to make money from an investment property:

What is needed to get investment property mortgage pre approval?

If you’ve had experience buying property, you’ll soon notice that lenders ask for the same types of information to pre-approve a mortgage on an investment property as they do for a primary residence.

At the bare minimum, a lender will want to know:

Lenders will use your social security number to perform a credit check to get your credit score and an idea of your credit history. At this stage, it’s likely you won't need to outline your debts because your credit reports will list the open loans and revolving credit accounts you currently have.

Qualification requirements for investment property pre approval

This is where you’ll find the major differences between pre-approval for a primary residence and an investment property.

From experience, lenders know that investment properties come with an added level of risk. When borrowers hit hard times they’re more likely to pay the mortgage for their primary residence than the mortgage for their investment property. In addition, tenants are less likely to pay the same level of attention and care to a rental property than an owner would if they were living in the home. For these reasons, the qualification requirements for investment properties are higher, and so are the interest rates.

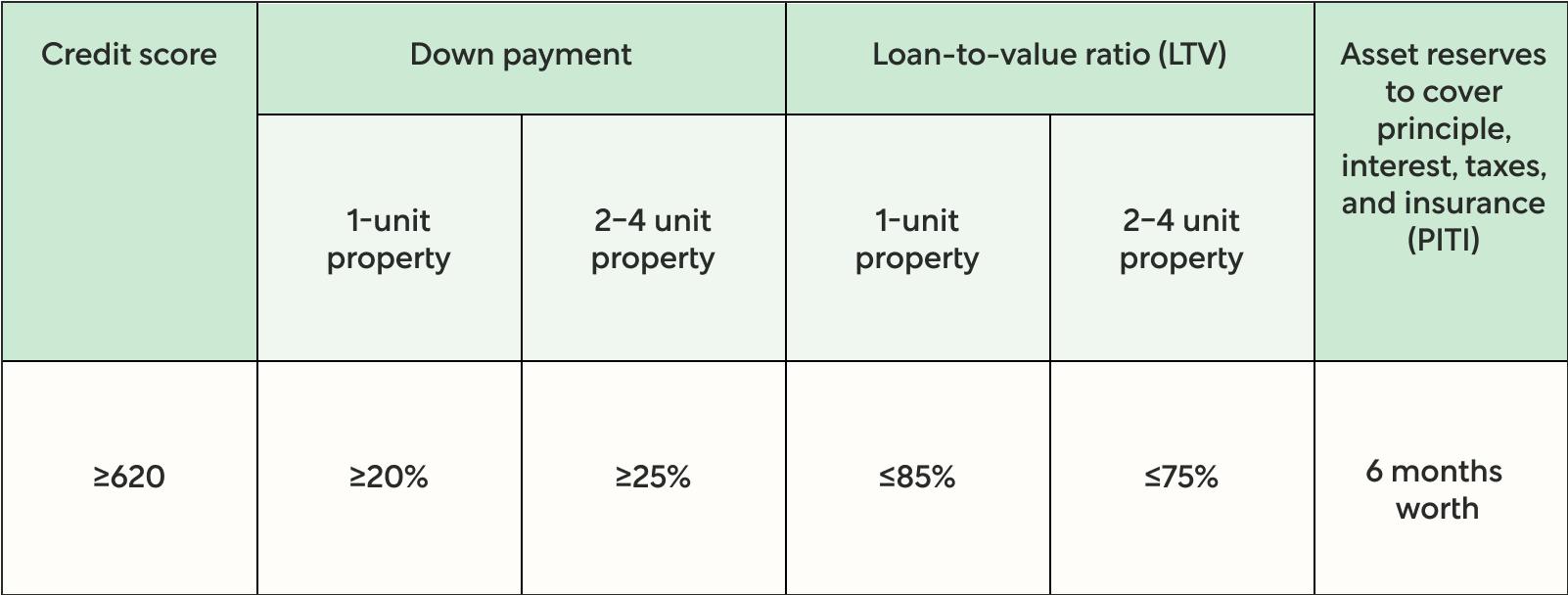

Minimum qualification requirements for an investment property mortgage*

*There may be some exceptions to these requirements for certain transactions. A licensed Better Mortgage Loan Consultant can give more detailed information tailored to your unique financial situation.

Understanding the costs associated with investment property mortgage pre approval

When seeking mortgage pre-approval for an investment property, it's important to account for additional costs beyond the mortgage itself. These costs can vary significantly depending on the type and location of the property, but here are a few key expenses to keep in mind:

Understanding these costs will give you a clearer picture of the financial commitment and help you better plan for a successful investment property purchase.

Mortgage pre approval is the first step to owning an investment property

If you’re curious to see if you qualify for your first investment property loan, get pre-approved with Better Mortgage. In as little as 3 minutes, you will get an idea of how much you can borrow and what interest rates you may qualify for.